The digital revolution has fundamentally reshaped the way customers engage with their finances

For financial institutions, from established private banks, like Julius Baer, and retail banks, similar to ING, to agile neo banks, like Revolut, launching a modern and highly engaging investing app is no longer optional.

It is now a core strategy for acquiring and retaining the next generation of wealth, especially in the fast-growing space of retail investing. This guide gives financial leaders a clear, professional framework to:

Understand the investing vs trading difference and what kind of client you really want to serve.

Decide whether to build your own investment app or partner for an execution-only investing platform.

Explore the benefits of a B2B white label investment platform like InvestSuite’s Self Investor.

What Is an Investment App?

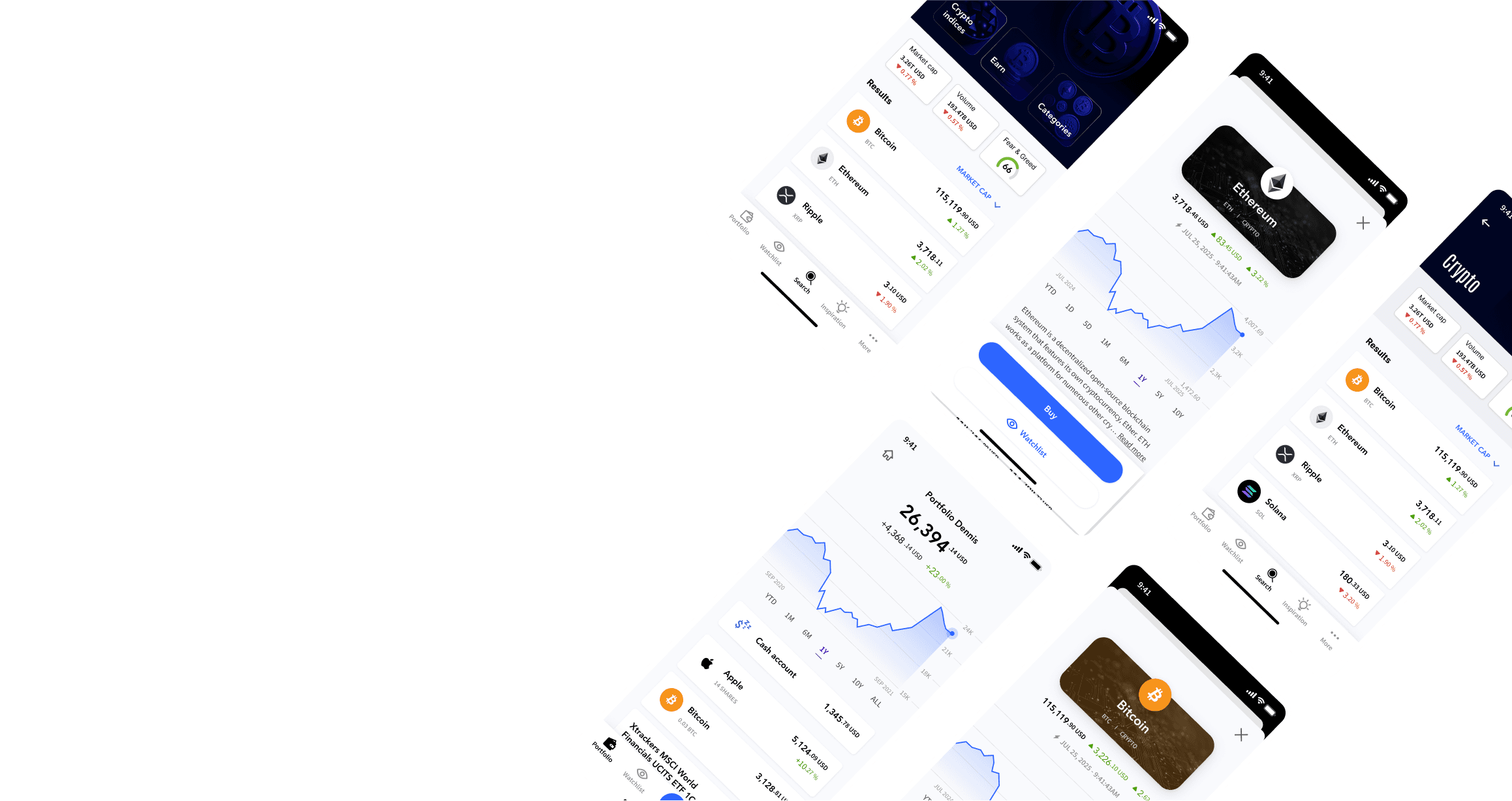

An investment app (or investment platform) is a sophisticated digital interface that serves as a crucial gateway between customers and the financial markets. It is designed to empower individual investors with the tools and access necessary to take control of their financial future. More than a trading tool, a modern investment app is a comprehensive ecosystem that digitizes the entire investment journey.

Its core functionalities allow customers to:

Execute Trades and Build Portfolios

The primary function is to facilitate direct investment in a wide array of financial instruments. This typically includes, but is not limited to, highly liquid assets such as individual stocks (equities) from major global exchanges, Exchange-Traded Funds (ETFs) that offer diversified exposure to various indices or sectors, mutual funds, and sometimes bonds/fractional shares, or even crypto assets, or options and other derivatives. The app handles the complexities of order routing and execution, making the process of buying and selling assets seamless.

Manage and Rebalance Portfolios

Investors are given the tools to view, analyze, and manage their entire investment portfolio independently. This includes features for understanding whether one is investing in line with one’s risk tolerance, and setting up automated regular investment plans (dollar-cost averaging). Advanced apps may also offer tools for tax-loss harvesting or automated dividend reinvestment.

Access Research and Educational Resources

To ensure customers make informed decisions, a value-add investment app often provides access to essential market data, including real-time quotes, charts, news feeds, analyst ratings, and company fundamentals. Furthermore, many platforms incorporate educational content, tutorials, to improve the financial literacy and confidence of their users.

For instance InvesSuite’s white-label investment platform Self Investor, has an Inspiration Tab that does just that – offers articles and investments overviews meant to inspire the app users to take a next financial step in the desired direction.

Investing vs Trading: What Type of App Should You Build?

The distinction between investing vs trading is central to your digital (wealth) strategy and determines the type of app your financial institution should launch.

Investment platforms focus exclusively on mid- to long-term investors, specifically excluding day traders. Here’s how an investment app differs from a trading app:

Feature

Investment App

(Long-Term Wealth)

Trading App

(Short-Term Speculation)

Customer Goal

Wealth accumulation, diversification and structured financial goals.

Short-term profits, market timing and exploitation of daily or weekly volatility.

Strategy

Systematic contributions, buy-and-hold, disciplined portfolio management.

Frequent trading, utilization of leverage to amplify bet sizes.

Product Focus

Core products like stocks, ETFs, mutual funds; sometimes with a side of derivatives products for the most sophisticated investors looking to hedge some of their risks.

Leveraged instruments (options, CFDs, futures, perpetual futures) and advanced order types.

Customer Profile

Individuals seeking financial serenity but who want to express a view on the market, typically retail and non-professional investors.

Traders or day traders, as well as professional investors.

By deploying an execution-only investing app focused on long-term investing, financial institutions help customers build wealth in a structured way that aligns with fiduciary responsibilities and the core banking values like financial education, financial inclusion, and responsible participation in the capital markets.

Why Banks Need an Investment App for (Retail) Investing

A branded investment app is now the most effective channel to attract and engage a modern client base that might otherwise go to in-market competitors (like Bolero) or international players such as Saxo, TradeRepublic, Revolut or Robinhood.

The shift in client behavior, particularly among younger generations, demands convenient, on-the-go access to financial services. A dedicated mobile application serves as a powerful tool, significantly lowering the barrier to entry for prospective investors, activating sleeping savings, increasing fee-based income, and reinforcing the institution's brand identity directly within their smartphone.

By providing this level of accessibility and control, financial institutions can dramatically increase client engagement, retention, and lifetime value. Furthermore, the investment app can be enriched with behavioural data with each use, representing a rich source of data which institutions can then leverage to personalize offerings, refine marketing strategies, and ultimately drive greater business growth in an increasingly competitive wealth management landscape.

Build Your Own Investing Platform from Scratch

Requires large CapEx and a dedicated in-house engineering team (possibly augmented by external forces during the “build” phase).

Often takes 2 years or more to reach production.

Carries high execution risk (especially if you’ve never done it before) and slower time-to-market compared to the alternative.

May require significant leadership to shift attention from the day-to-day of the current core business.

Use a B2B White Label Investing Platform

For most financial institutions, the more practical choice is to partner with a provider of a B2B white label investing platform, such as InvestSuite:

Converts heavy CapEx into predictable operational costs (OpEx).

Dramatically reduces development time; go live in just a few months instead of years.

Allows quick access to an all-rounded expert team.

Leverages a proven technology stack, already designed for retail investing use cases, and already in production.

Allows you to launch your own branded execution-only investing platform while keeping control over the client relationship.

IIf you are interested in finding out more about this topic, you can check out our dedicated article on the topic: White-label or in-house? How banks decide on WealthTech Platforms.

What Is a White Label Investing Platform?

A white label investment platform is a comprehensive, ready-made, connection-agnostic, technology solution meticulously designed and developed by a specialized provider. This platform is then offered to financial institutions, such as banks, wealth managers, and neobanks, which can fully brand it, integrating it seamlessly into their existing digital ecosystem and presenting it to their end-clients as their own offering.

This approach allows financial institutions to rapidly launch or upgrade their investment services, like execution-only trading (or robo-advisory, as you can see in our other articles), without the time, expense, and risk associated with building a platform from scratch.

This operates within a B2B model, where a technology provider supplies the core infrastructure, software, enabling the financial institution to act as the direct distributor of investment products and services.

In this B2B model:

The Technology Provider (Vendor): Develops, maintains, updates, and ensures the security and configuration of the underlying platform infrastructure (e.g., API layers, order processing, and core user interface components). They are the experts in wealthtech development and technology.

The Financial Institution (Client): Licenses the platform, applies their corporate branding, manages the client relationship, defines the product offering (which assets to trade, fee structure), and holds the necessary regulatory licenses to interact with and manage client orders, assets and accounts.

Some of the advantages of a White Label Investment Platform include:

Rapid Time-to-Market: One of the many advantages for the financial institution is the speed at which they can launch new digital investment services. Instead of spending multiple years on development, they can often go live in a matter of a few months.

Reduced Development Cost and Risk: The institution avoids the massive upfront capital expenditure, some of the ongoing operational costs, and inherent risks (technology failure, keeping up with new feature development) associated with internal software development.

Focus on Core Competency: The financial institution can dedicate its resources and strategic focus to client acquisition, relationship management, and financial product innovation, leaving the complex, non-core technology roadmap and maintenance to the specialist vendor.

This B2B investment platform approach enables banks to offer a state-of-the-art investing app without becoming a specialized, world class, investment-software company.

InvestSuite’s Self Investor: A White Label Investment Platform to Consider?

Self Investor by InvestSuite is an example of a B2B white label investing platform designed specifically for financial institutions. Self Investor by InvestSuite stands as a premier example of a B2B white label investing platform specifically engineered for financial institutions looking to offer modern, scalable investment services to their clients.

This platform is designed to be fully integrated into the financial institution's existing digital ecosystem (broker/custodian, data providers, cloud/on-premise...), allowing them to maintain its brand identity (hence "white label") while leveraging InvestSuite's technology and investment expertise.

Key aspects of a solution like Self Investor include:

Core Execution-Only Functionality

Execution-only platform built for retail investing.

Intuitive, user-tested, easy-to-use interface for end clients.

Supports straightforward self-directed investing.

Adds value with inspiration, custom content, asset analysis, and much more.

Support for fractional shares, when the executing broker supports it.

Institutional-Grade and Future-Proof Technology

Built with institutional-grade infrastructure in mind, the InvestSuite Self Investor can be deployed on a cloud of your choice (Azure, Oracle, AWS, GCP) or on-premise, allowing you to enjoy the benefits of your investments in cyber security.

Designed for scalability, reliability and security.

Value Beyond Software

InvestSuite provides more than just software:

Support with analytics and performance measurement.

Assistance with go-to-market strategies and collateral

Application monitoring (L2) and Application support (L3) so you’re never on your own

Preventive and Corrective maintenance.

Evolutive maintenance with continuous market and user research for product development

Proven Client Success

Self Investor is currently being leveraged by leading players in the banking sector, such as the Commercial Bank of Dubai (CBD) By integrating InvestSuite's robust and scalable tools, these institutions are able to power their sophisticated, modern digital investment offerings, providing their clients excellent and accessible execution-only investment experiences.

Conclusion: What’s the deal with the investing apps?

The shift in retail investing requires financial institutions to deliver modern, seamless, mobile-first digital channels.

By adopting a B2B white label investing platform such as InvestSuite’s Self Investor, you benefit from:

Fast time-to-market for your own branded and highly configurable execution-only investing app

Scalable, secure, institutional-grade technology

Reduced complexity and operational burden

Forward-looking product roadmap and continuous innovation

This allows you to deploy a high-impact investment app swiftly and focus on what you do best: serving clients, and driving sustainable growth.

Would you like to explore how Self Investor fits into the broader InvestSuite portfolio of digital wealth solutions, such as our Robo Advisor or StoryTeller, and how they can work together in your digital strategy? Then don’t hesitate to schedule a demo with one of our experts to find out more!

FAQ

What is an execution-only investing app?

What is the difference between investing and trading?

Why should a bank use a white label investment platform?

Who is a retail investing customer?

Should we build our own investing platform or use a B2B investment platform?

What is a white label execution-only investment platform?

How does a white label investing platform work for banks and brokers?

What are the main benefits of an execution-only investing app for financial institutions?

How is a B2B investing platform different from a direct-to-consumer app?

Is an execution-only investing platform suitable for all types of investors?

How does a white label investment platform help with time-to-market?

What are the key features to look for in an execution-only investing platform?

How does a white label execution-only platform handle regulation and compliance?

Can a white label investing platform support multiple markets and asset classes?

How does a B2B investment platform integrate with existing banking systems?

What is the difference between a robo-advisor and an execution-only investing app?

How can an execution-only investing app support long-term investors?

What are the typical costs of using a B2B investing platform versus building in-house?

Can we still differentiate our brand with a white label platform?

Please complete the form below and one of our experts will contact you to make further arrangements.

Looking forward to connect!